CRAFTING JOURNEYS

Personalised Interactions

Professional Services

|

Financial Services

|

Personal Banking

|

Unsecured Loans

|

Customer Experience

|

Omnichannel Experience

|

Micro Moments & Journeys

|

Research

|

Design

|

UX

|

IA

|

Ideation

|

Prototype

|

App Design

|

Professional Services | Financial Services | Personal Banking | Unsecured Loans | Customer Experience | Omnichannel Experience | Micro Moments & Journeys | Research | Design | UX | IA | Ideation | Prototype | App Design |

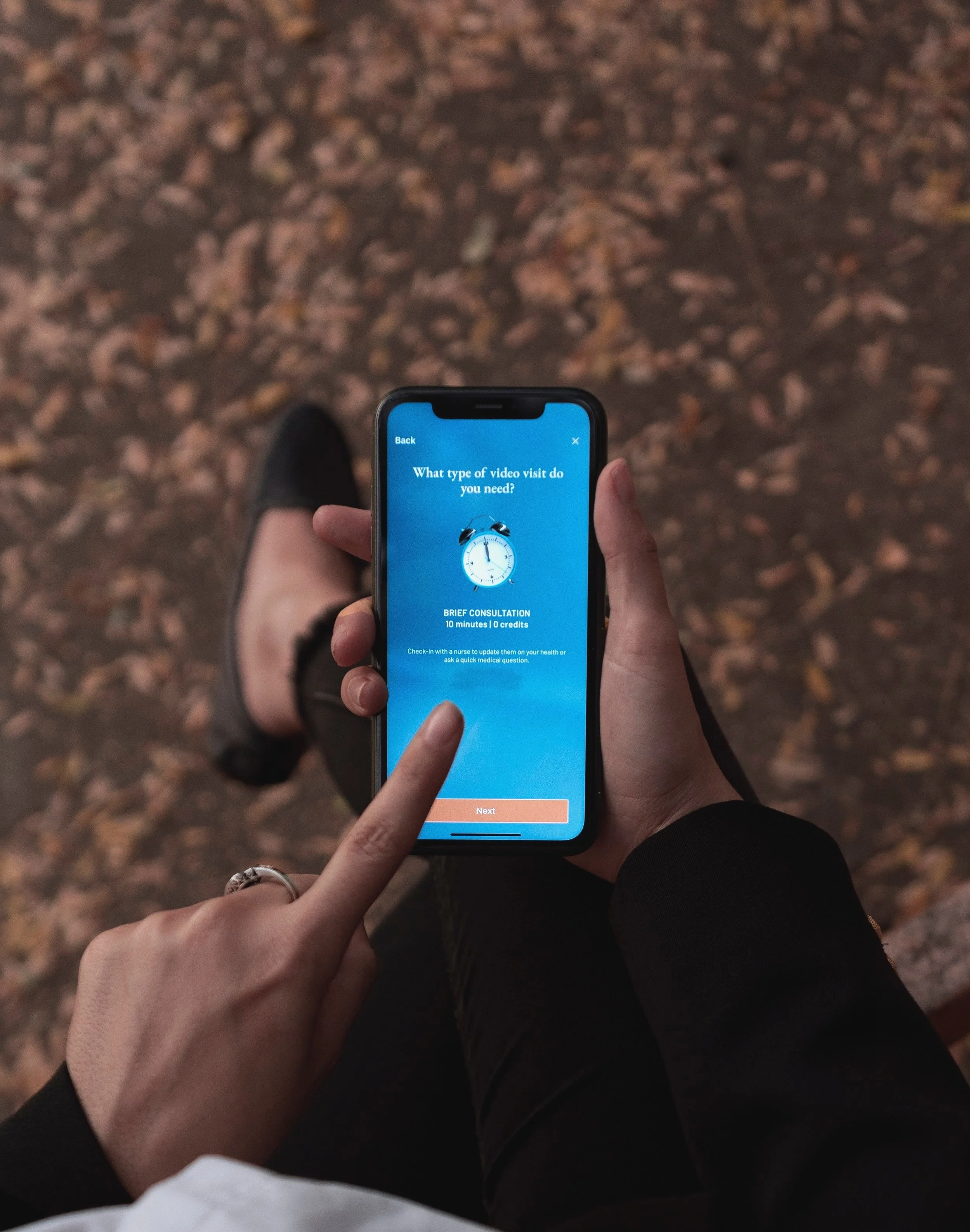

Deep diving into micro-moments across customer touchpoints is essential to understand nuanced behaviour. By investigating communication channels, interfaces and interaction points, we can attribute customer frustration and breakdowns to specific moments in key task flows, whilst understanding why they occur when speaking to people.

In personal banking, money mindsets matter. In 2022, Australians borrowed approximately $2.5 billion per month in new personal loans. The average loan amount was $22,643, at an average interest rate of 13.87% per annum. A significant portion of this borrowing can be attributed to the growing demand for credit lines without resorting to traditional methods. Lenders, such as traditional banks, evaluate an individual’s cash flow history and their ability to repay loans.

Unsecured loans do not require collateral, making them accessible to a broader range of borrowers, including those looking to improve their credit scores. The application process for these loans is quick, and they offer flexibility in usage, various loan types, and an array of rewards, which appeal to many individuals. When faced with urgent expenses, borrowers often overlook the higher interest rates associated with lending.

These loans were intended to provide customers with quick solutions to purchase essentials and fulfil desires. However, several factors such as the rise of consumerism, the glorification of social media bragging, influencer marketing, and the advent of open banking have left younger customers in financial distress, often due to poor money management skills. Budgeting and maintaining a positive relationship with finances have significantly declined.

With the introduction of open banking, a myriad of services have emerged in the financial sector. Money management has become increasingly important, and we have seen the rise of "Buy Now, Pay Later" (BNPL) models that exacerbate issues related to reckless spending, while traditional banks and credit unions continue to profit from these types of loans.

This is where the neo banks come in, aiming to help people better understand their spending habits, limit their use of credit, inspire saving, and encourage positive financial behaviours. They provide categorised spending breakdowns, goal-setting tools, budgeting features, investment opportunities, and round-up saving options.

As a result, traditional lending institutions need to adapt, innovate, evolve and step up their game…

Engagement Details

-

We identified engagement drop-offs from data sources in multiple areas and moments in key customer task flows. From the metrics available from the NPS, market scan, benchmarking and Personal Banking lending (credit/debit card and unsecured loans) data, we were able to compile hypotheses of trends, patterns and anomalies. We sought to dig a little deeper to understand where the touchpoints were that inhibited usage and less-than-desirable moments for customers.

The key areas we sought to explore were throughout the entire customer journey.Awareness

Acquisition

Activation

Action

Assistance

Advocacy

BUSINESS GOALS

Cluster, prioritise and address feedback made available from NPS surveys

Identify areas where users might be frustrated or have a negative experience and understand why they occur

Spot trends that might indicate declining user satisfaction which potentially lead to cancellations

Observe loyal users who are likely to recommend the app to others, providing valuable word-of-mouth marketing

Seek valuable insights to improve app design, functionality, and overall user experience

-

We made enhancements throughout customer touchpoints, the digital channels to provide a personalised and consistent pathway to better money habits. Identifying the service modelling along with intricate details about the current and optimal solution journeys.

The key things we wanted to ensure customers could achieve were:

Understand their current income, assets and revenue streams with effective data visualisation techniques

Learn about their expenditure, bills, spending habits with accurate reporting

Uncover their balance and financial positioning, highlighting their spending patterns

Specify their financial goals and set targets with actionable recommendations

Budget and automate transactions over a nominated period accommodating for change

Reflect and reshape future ambitions

-

We made significant omnichannel enhancements increasing acqusition of new customers, an improved NPS, greater trust scores and feedback in surveys conducted. App installations had gradually risen over the course of 3 months post-change as well as an re-engagement increase of non-active account holders.

We asked, acknowledged, addressed and acted on customer feedback to ensure a seamless integration from simple daily tasks to those challenges which come with greater complexity.

-

xxxx

xx

xx

xx

xx

xx

xx

xx

xx

xx

xx

xx

xx

xx

xx

Observations

xx

xx

xx

Actions

xx

Defer to the next iteration

Pursue organisation chart customisation with custom coding

Gallery

View Examples

•

View Examples •